Is your stockbroker charging you too much? Has your financial adviser saddled you with investments that are not helping you reach goals? Is your health insurance policy low on benefits and high on premium? Maybe it's time you considered switching financial service providers.

Thanks to changes in the financial services arena, shifting from one service provider to another is no longer complicated. But while choice is good, switching to other alternatives requires careful deliberation. In this story, we guide you through some of the options to consider, should you decide to junk your existing service provider and embrace another.

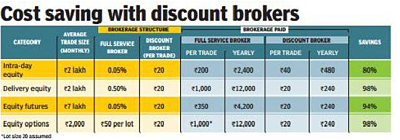

Your stockbroker The choice of service providers in the stockbroking space has multiplied with the mushrooming of discount brokers who offer no-frills accounts. You get the basic trading facility at a fraction of the cost of 'full-service' brokerages, which apart from helping you buy and sell shares, offer add-ons like research reports, advisory and a relationship manager. However, frequent traders often find the hefty brokerage charged by traditional brokers eating up their profits. Discount brokers thus help you shave off up to 90% of brokerage costs incurred with full-service brokers. They charge a fixed brokerage per trade across stocks, currency and commodities. The amount you shell out remains the same irrespective of size of trade.

Whether you should opt for a discount broker or not would depend on your comfort and level of knowledge in dealing with the stock market, the frequency and size of trades, your trading requirements as well as how tech-savvy you are. With a discount broker, you need to know your way around the market.

For a newbie investor, a traditional broker may work better. They provide higher margin funding or 'leverage'— you borrow money from the broker to purchase shares—compared to a discount broker. Those who prefer the 'call and trade' facility will find that a discount broker charges extra for each executed order. Also, if you need access to a wider range of products, a traditional brokerage would serve you better as they facilitate investments in other products like mutual funds, NCDs, tax-free bonds and fixed deposits. Apart from the flat rate structure, most traditional brokerages also offer volume-based plans where the brokerage varies according to the size of transactions on a periodic basis. At higher turnovers, the brokerage can come down to as low as 0.05-0.15%. However, while beginners may benefit from the handholding, they must not rely too much on trading tips from the traditional broker. Executing trades on the basis of such ideas only drums up trading volumes for the tip giver.

Discount brokers, on the other hand, can be beneficial for seasoned traders who execute trades frequently and understand market dynamics. The low, flat brokerage structure proves very costeffective at higher trading volumes and higher transaction size. Let us assume you carry out five different transactions through a full-service broker totalling `1 lakh in a month. You will end up paying a brokerage of `300 to `500 on these trades at 30-50 paisa per `100. But the same transactions through a discount broker will cost `45 to `100. Some discount brokers even charge zero brokerage for transactions in the cash (delivery) segment, while some offer 'unlimited trading' at a flat monthly charge of as low as `999. For those who can do without add-ons, this cost saving is reason enough to open an account with a discount broker.

Your financial adviser

A well thought-out financial plan can go a long way in ensuring all your life goals are met. A dedicated financial planner can help chart out a roadmap by making smart investment choices and timely corrective measures in your portfolio. However, there is a dearth of quality, unbiased advice on offer. Many will peddle products that fetch them fat commissions even if they do not suit your risk profile or portfolio. So, what are your options?

Move to a 'fee-only' planner

Investors have the choice of consulting an adviser paid by the product manufacturer or paying the adviser an upfront fee without him getting a penny from the manufacturer. The latter are the new breed of 'fee-only' advisers who will not force you to buy products they recommend. These registered investment advisers (RIA) are allowed to earn income only by way of fees—either a flat retainer or a certain percentage of corpus size—from clients and not through commissions. The argument in their favour is that they are more likely to recommend products that would best fit the client's needs rather than those that fetch them a fat commission. The adviser's thrust here is on building a long-term relationship based on trust. He will be in a position to offer you direct plans of mutual funds, which charge a much lower expense ratio as they do not incur costs of commission to the intermediary.

This is not to say that commissionbased advisers do not do honest work. There are plenty who are actively engaged in educating the client and not just making money off them. If you see value in their services and find yourself progressing under their guidance, there is no need to grudge them the commission. Try and ascertain at the outset how much commission the adviser stands to pocket when you invest in products he recommends.

Consider robo-advisory

These online wealth management services provide automated, algorithmbased advice without any human intervention, at a fraction of the cost. Arthayantra, FundsIndia, Scripbox, MyUniverse and 5nance are some prominent players. Except Arthayantra, all others operate on the commission model. They help you plan your life goals by designing a curated portfolio of mutual funds or more. However, robo-advisers do not offer holistic solutions and cannot customise beyond a point. But they are a good starting point for investors who do not have access to quality financial advice.

Your health insurer

Have you bought health insurance cover outside of your employer provided mediclaim policy? If yes, you have made the right move. But there is a chance that you have bought a policy that is not the best fit for you. If you are dissatisfied with your insurer or policy in any way, switch insurer under the health insurance portability norms laid down by Irdai. These allow you to port existing policy at the time of renewal while holding on to benefits accrued with the previous insurer. It also allows you to customise the new policy for added benefits.Those covered under an employer group health policy can also request porting to an individual policy, but with the same insurer.

There are no extra charges for porting; you only pay the premium applicable on the new policy. Most health policies come with a waiting period of 2-3 years after which certain pre-existing health conditions are covered. If the policy is transferred to another insurer, the waiting period completed with the existing insurer is counted. Even if the new insurer requires a longer waiting period, the policyholder need only wait for the remaining time period. The continuity in policy benefits also applies in case of waiting period for certain surgeries. In most cases, the sum assured under the existing policy is added to any accrued bonus, to give the new sum assured, and premium is charged accordingly.

Read more